Infographic: Ather Energy Hits Record High as Q4 Loss Shrinks and Revenue Soars

Ather Energy Stock Surges to All-Time High on Strong Financial Performance

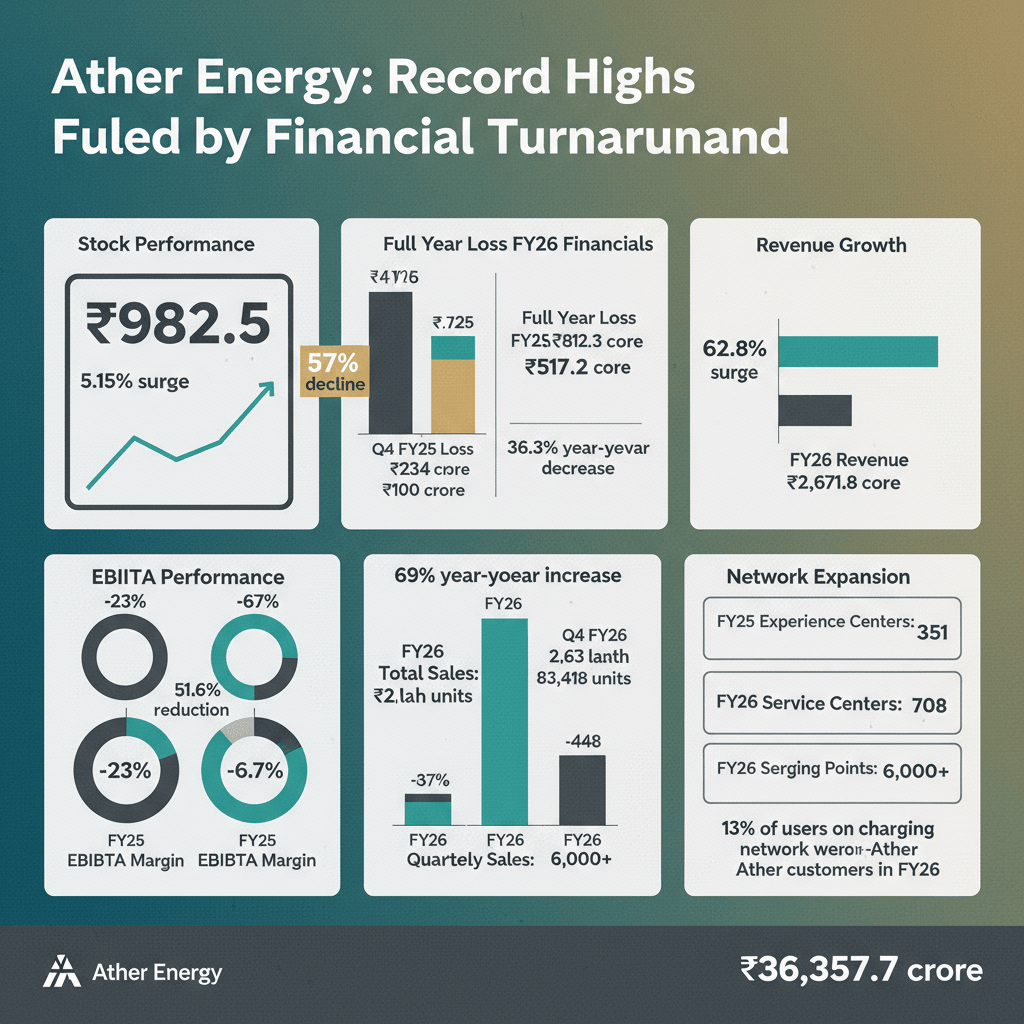

Ather Energy’s stock experienced a significant surge, climbing as much as 5.15% to touch an unprecedented all-time high of ₹982.5 on the Bombay Stock Exchange (BSE). This upward momentum was fueled by positive investor sentiment, largely attributed to the electric vehicle manufacturer’s improved financial performance in the fourth quarter of the fiscal year 2026 (Q4 FY26). While the stock later saw some moderation, it continued to trade higher, reflecting sustained investor interest.

The company’s market capitalization reached approximately ₹36,357.7 crore (around $3.8 billion) during the trading session. This impressive valuation underscores the market’s growing confidence in Ather Energy’s growth trajectory and its strategic positioning within the rapidly expanding electric two-wheeler sector.

Significant Reduction in Q4 FY26 Loss and Robust Revenue Growth

The primary driver behind the stock’s rally was Ather Energy’s announcement of a substantial reduction in its financial losses for FY26. The company reported a 36.3% year-over-year decrease in its full-year loss, which narrowed to ₹517.2 crore from ₹812.3 crore in FY25. This improved profitability is a key indicator of the company’s operational efficiencies and cost management strategies.

In the specific fourth quarter ending March 31, 2026, Ather Energy’s loss stood at ₹100 crore, marking a significant 57% decline compared to the ₹234 crore loss recorded in the same period of the previous year. This sharp reduction in quarterly losses highlights the company’s ability to navigate market challenges and improve its bottom line.

Strong Top-Line Performance and Margin Improvement

Beyond loss reduction, Ather Energy also showcased impressive top-line growth. Operating revenue for the full fiscal year FY26 surged by 62.8% to ₹3,671.8 crore, a substantial increase from ₹2,255 crore in the prior fiscal year. This revenue expansion reflects strong demand for Ather’s products and successful market penetration strategies.

The company also made strides in improving its operational profitability, evidenced by a 51.6% reduction in its Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) loss, which came in at ₹257 crore. Consequently, the EBITDA margin improved to -6.7% from -23% in FY25. In Q4 FY26, the EBITDA loss was further reduced to ₹30 crore, with the margin improving to -2.5% from -23.3% in the year-ago quarter. Revenue during the quarter saw a remarkable year-over-year jump of 73.7%, reaching ₹1,174.7 crore, with a sequential growth of 23.2%. Including other income, the total income for the quarter stood at ₹1,213.8 crore.

Record Sales Volumes and Network Expansion Drive Growth

Ather Energy’s sales performance has been a significant contributor to its financial success. The company sold a record 2.63 lakh units in FY26, representing a 69% year-over-year increase. The fourth quarter of FY26 was particularly strong, with the company clocking its highest-ever quarterly sales of 83,418 units. This exceptional sales growth is attributed to strategic expansion across various geographies, a broadening retail network, and robust consumer demand, particularly for its family scooter, the Rizta.

Complementing its sales growth, Ather Energy has aggressively expanded its retail and service footprint. The number of experience centers nearly doubled, reaching 700 by the end of FY26, up from 351 at the end of FY25. The service network also scaled up to 548 centers, and the charging network surpassed 6,000 points. Notably, the company observed that approximately 13% of the users on its charging network were non-Ather customers in FY26, indicating a broader utility and reach of its infrastructure.

Navigating Supply Chain Challenges and Strategic Battery Choices

The company acknowledged that its production was partially impacted in Q2 and Q3 of FY26 due to China’s export restrictions on rare earth magnets. Furthermore, Ather Energy made temporary adjustments to its manufacturing processes, which led to the deferral of ₹24.5 crore worth of incentives to a later period, as these adjustments did not fully align with India’s Phased Manufacturing Programme norms.

Facing pressure from rising lithium-ion battery prices, exacerbated by global supply constraints and strong demand, Ather Energy strategically introduced lithium iron phosphate (LFP) batteries. This move aims to enhance flexibility and drive cost efficiencies in its battery supply chain, a critical component for EV manufacturers.

Positive Brokerage Outlook Reinforces Investor Confidence

Following the release of its strong financial results, major brokerage firms have reiterated their positive outlook on Ather Energy. HSBC maintained a ‘Buy’ rating with a target price of ₹1,050, acknowledging potential delays in profitability timelines due to commodity headwinds but emphasizing the company’s robust long-term investment case, supported by its strong brand equity and execution capabilities.

Nomura also upheld a ‘Buy’ recommendation, setting a target price of ₹1,120. The brokerage cited strong growth visibility and identified Ather Energy as a top pick in the electric two-wheeler segment. Nomura anticipates that new platform launches and continued network expansion will be key drivers for volume growth, even as margins may face near-term pressure.